Unit Boundaries vs. Standard Unit Definitions

Today I thought I would write about a common misconception in the industry about a condominium’s documents. It is something that I’ve heard frequently as of late, so it seemed a good idea to post about it again. Some people believe that a standard unit by-law is the same as the unit boundaries found in the declaration (typically in “Schedule C”). Sometimes people believe the standard unit by-law can change the unit boundaries. None of this is true. The documents have different purposes and cannot be used interchangeably.

Unit Boundaries

To create a condominium the declarant must register both a declaration and a description (the “condo plan”) that contain certain prescribed information, including a description of the boundaries of the units. If an item is not within the unit boundaries it forms part of the common elements (or exclusive use common elements). For newer condominiums the unit boundaries are described in Schedule C. For older condominiums (pre-2001) the unit boundaries may be defined in other schedules or the body of the declaration.

Standard Unit Definitions

Section 99 of the Condominium Act, 1998, requires condominiums to maintain insurance for damage to the units and common elements that is caused by major perils or other perils the declaration or by-laws specify. This applies to standard condominiums (including those with lot line or whole lot unit boundaries), but not to common elements or vacant land condominiums (See s.144 of the Act for common elements condominiums and s.159 for vacant land condominiums for the exemption from this requirement to insure the units).

The condominium’s obligation to insure the units does not include improvements made to the units. How do you establish what constitutes an improvement to a unit? That could be exceptionally difficult with a 30-year-old unit that has been renovated several times. Fortunately, the Act allows a condominium to define what is standard and what is an improvement. Subsection 99(5) states there are only two ways:

- pass a by-law defining the standard unit; or

- a schedule defining the standard unit provided by the declarant on turnover.

The purpose of these by-laws is to determine the responsibilities for repairing the improvements to the units after damage and insuring them. If an item is included in the standard unit definition, the condominium is responsible for insuring it. If an item is excluded from the definition, it is an improvement and the owner is responsible. It is important to note that the standard unit definition created by by-law or a schedule from the declarant does not need to match what was constructed. For example, most standard units do not include flooring materials, despite the units being constructed with carpet, tile, etc.

What’s the Difference?

The way I normally explain the difference is this: the declaration and description describe the physical boundaries of the unit (what the owner owns vs. what is shared by all owners). The standard unit defines who insures the various components of the unit that the owner owns.

This does not mean that you can ignore Schedule C when creating a standard unit by-law or schedule from the declarant. The standard unit by-law will start with the unit boundaries from Schedule C and define the materials included in the standard unit definition. For example, the unit boundary is often the “backside of the drywall” which means the unit includes the drywall. A standard unit by-law could not change the boundary to exclude the drywall from the unit. That could only be achieved by amending the declaration and description. However, the standard unit by-law could indicate that the standard unit includes the drywall, in which case the condominium would be responsible for insuring it. Alternatively, the standard unit by-law could exclude the drywall from the standard unit (meaning it is an “improvement” to the unit), in which case the owners would be responsible for insuring it. Perhaps looking at some sample language would help explain this.

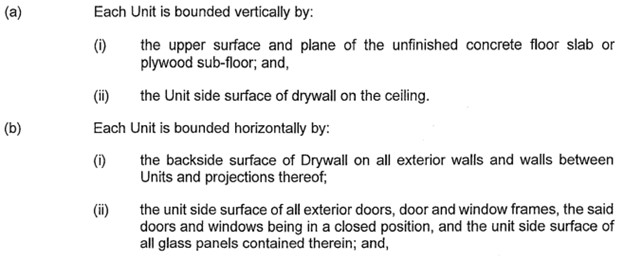

Here is a portion of Schedule C from a declaration:

The excerpt above tells owners that their unit includes the drywall on the walls in their unit (see use of backside surface of drywall above), but not the exterior doors and windows (see unit side surface above).

The standard unit by-law for this same condominium may state something like this:

Why Does it Matter?

Without a standard unit definition there is a great deal of uncertainty as to what is standard and what is an improvement, meaning the condominium’s obligation to insure the standard unit and the owner’s obligation to insure the improvements are also unclear. Schedule C of the declaration on its own does very little to help figure this out. As in our example above, Schedule C might let us know the unit includes drywall, but it does not tell us the thickness of that drywall, or whether it includes the taping, sanding, priming, and painting that is typically applied to the drywall.

If neither the condominium nor the owner’s insurers know what is standard and what is improvement, they will likely both over insure the units. Or, even worse, the condominium or owner may have under insured the unit because they assumed the other was responsible for insuring it. This could be disastrous if substantial damage occurs to a unit, resulting in the potential for large special assessments to repair the damage if the condominium has not adequately insured the unit.

As always, if you have any suggested topics, please let us know.